Receiving a Canada IRCC PFL for a suspected fake bank statement can feel overwhelming, especially in 2026 where immigration checks are stricter than ever. With advanced verification systems and direct bank validation, even small financial inconsistencies are quickly flagged by IRCC, making proof of funds one of the most sensitive parts of any application.

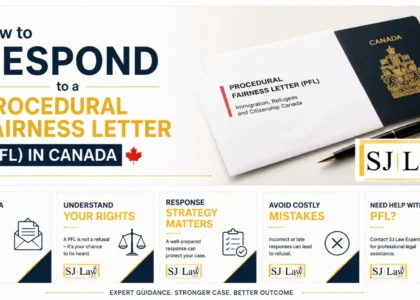

However, a Procedural Fairness Letter is not a refusal, it’s your chance to respond and defend your case. The key lies in providing a clear, honest, and well-documented explanation that addresses IRCC’s concerns directly. A strong response can still protect your application and prevent serious consequences like refusal or a long-term ban.

Why IRCC Issues a PFL

The Canadian immigration system is strict about transparency and honesty. Officers don’t issue a Canada IRCC PFL randomly, it happens when there’s a serious red flag in your application.

Here are the most common triggers:

- Suspected fake or altered documents

- Inconsistent financial records

- Unverifiable employment or funds

- Large unexplained bank deposits

One of the biggest reasons is proof of funds issues, especially when bank statements don’t match financial history. When IRCC suspects something isn’t right, instead of rejecting your application immediately, they give you a chance to clarify. That’s where the PFL comes in.

Fake Bank Statement Issues in Immigration Applications

Why Proof of Funds Matters

Let’s be honest, immigrating to Canada isn’t cheap. The government wants to ensure you can support yourself without relying on public funds. That’s why proof of funds is a critical requirement.

For study permits, PR applications, or visitor visas, your financial documents must:

- Be genuine

- Show consistent balance

- Reflect a clear source of income

If your bank statement looks manipulated, it raises immediate suspicion.

How IRCC Detects Fake Bank Statements

You might be wondering, how does IRCC even know if a bank statement is fake?

Here’s the surprising part: they have advanced verification methods.

- Direct bank verification

- Cross-checking transaction patterns

- Reviewing sudden deposits

- Comparing documents across applications

If something doesn’t add up, they flag your case and issue a Canada IRCC PFL. Even a small inconsistency can lead to serious consequences. And yes, many applicants from Pakistan face this issue due to reliance on unverified agents.

Common Reasons Pakistan Applicants Receive Canada IRCC PFL

Misrepresentation Concerns

Misrepresentation is one of the most serious allegations in Canadian immigration. It includes:

- Submitting fake bank statements

- Providing incorrect financial data

- Hiding important information

Even if it wasn’t intentional, IRCC may still treat it as misrepresentation.

Sudden Bank Deposits

Imagine this, you submit a bank statement showing a large amount deposited just a few days before applying. That’s a red flag.

IRCC often questions:

- Where did the money come from?

- Is it genuinely yours?

- Was it borrowed temporarily?

If you can’t explain it properly, you’ll likely receive a Canada IRCC PFL.

Third-Party Agents Mistakes

This is extremely common in Pakistan.

Many applicants trust agents who:

- Edit bank statements

- Inflate balances

- Submit fake documents

And here’s the harsh truth: you are still responsible, even if the agent made the mistake.

Legal Consequences of Fake Documents

Under Canadian immigration law, submitting false documents is classified as misrepresentation.

This includes:

- Fake bank statements

- Altered financial records

- Misleading financial history

Even accidental errors can fall under this category if they affect decision-making.

5-Year Ban Risk

Here’s where things get serious.

If IRCC concludes that you committed misrepresentation:

- Your application is refused

- You may be banned from Canada for 5 years

That’s not just a delay, it’s a complete shutdown of your immigration plans.

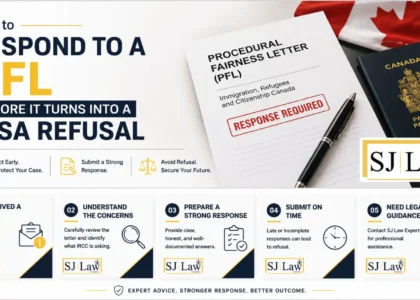

How to Respond to Canada IRCC PFL Effectively

Step 1: Understand the Allegation

Don’t rush. Read the letter carefully.

Identify:

- What exactly IRCC is questioning

- Which documents are under suspicion

- The deadline to respond

A misunderstanding here can ruin your case.

Step 2: Gather Strong Evidence

Your response must be backed by proof. This may include:

- Original bank statements

- Bank verification letters

- Income proof

- Transaction history

If your documents are genuine, proving it is your strongest defense.

Step 3: Write a Professional Explanation Letter

This is your chance to tell your side of the story.

Your explanation should be:

- Clear and structured

- Honest and factual

- Supported by documents

Avoid emotional language. Stick to facts.

Step 4: Submit Within Deadline

- Deadlines are strict, usually 7 to 30 days.

- Missing the deadline almost guarantees refusal.

Best Defense Strategies for Fake Bank Statement Cases

If You Are Innocent

If your bank statement is genuine:

- Get official verification from your bank

- Provide stamped and signed documents

- Include transaction history

Prove authenticity beyond doubt.

If There Was a Mistake

Mistakes happen. Maybe you uploaded the wrong file or there was confusion.

In this case:

- Admit the mistake

- Provide correct documents

- Explain clearly

Honesty can sometimes save your case.

If an Agent Submitted Fake Documents

This is tricky, but still defendable.

You should:

- Explain your reliance on the agent

- Provide original genuine documents

- Show lack of intent

But remember, this defense is not always successful.

Documents You Should Provide in Your Response

Here’s what strengthens your case:

- Original bank statements

- Bank-issued verification letter

- Source of funds proof (salary slips, business income)

- Affidavit explaining situation

- Any communication with agent

The stronger your evidence, the better your chances.

Mistakes to Avoid While Responding to PFL

Let’s be real, many applications fail not because of the issue, but because of a poor response.

Avoid these:

- Ignoring the PFL

- Submitting fake documents again

- Giving vague explanations

- Missing deadlines

- Being overly emotional

A PFL response should feel like a legal defense, not a personal rant.

Role of Immigration Lawyers (SJ Law Experts)

This is where professionals make a difference. Handling a Canada IRCC PF, especially for fake bank statement cases, is complex. A small mistake can cost you years.

SJ Law Experts specialize in:

- Drafting strong PFL responses

- Building evidence-based defense

- Handling misrepresentation cases

- Increasing approval chances

Think of them as your defense team. When the stakes are this high, going alone isn’t always the smartest move.

Real Case Scenarios and Outcomes

Let’s look at realistic outcomes:

| Scenario | Response Quality | Outcome |

| Genuine funds, strong proof | Excellent | Approved |

| Weak explanation, no proof | Poor | Refused |

| Fake documents confirmed | None | 5-year ban |

| Agent mistake, strong defense | Good | Possible approval |

Your outcome depends heavily on how you respond.

Tips to Avoid PFL in Future Applications

Want to avoid this nightmare altogether?

- Never submit fake documents

- Avoid unreliable agents

- Maintain consistent financial history

- Keep proper records

- Double-check everything before submission

Prevention is always easier than defense.

Conclusion

Receiving a Canada IRCC PFL for a fake bank statement is serious, but it’s not the end of the road. It’s your final chance to defend your case and prove your credibility. What matters most is how you respond. A strong, evidence-backed explanation can save your application, while a weak or careless response can lead to refusal, or worse, a 5-year ban. If you’re facing this situation, don’t panic. Focus, prepare, and respond strategically. And if needed, seek professional help like SJ Law Experts to maximize your chances.

FAQs

1. What is a Canada IRCC PFL?

A Canada IRCC PFL is a letter issued by immigration officers when they have concerns about your application and want your explanation before making a decision.

2. Can I still get approval after a PFL?

Yes, many applicants get approved if they provide strong evidence and a clear explanation.

3. What happens if I ignore a PFL?

Ignoring it usually leads to refusal and possibly a ban.

4. How long do I have to respond to a PFL?

Typically between 7 to 30 days, depending on the case.

5. Can an agent’s mistake cause a ban?

Yes, even if an agent made the mistake, you are responsible for your application.